|

However the scars of the crisis are still visible in the American housing market, which has actually undergone a pendulum swing in the last years. In the run-up to the crisis, a housing surplus triggered home mortgage lending institutions to issue loans to anybody who might mist a mirror just to fill the excess inventory. It is so strict, in reality, that some in the realty market believe it's adding to a real estate scarcity that has actually pressed house rates in a lot of markets well above their pre-crisis peaks, turning more youthful millennials, who matured during the crisis, into a generation of renters. "We're really in a hangover phase," said Jonathan Miller, CEO of Miller Samuel, a realty appraisal and seeking advice from company. [The marketplace] is still distorted, which's since of credit conditions (what kind of mortgages do i need to buy rental properties?)." When loan providers and banks extend a home loan to a property owner, they usually don't generate income by holding that home mortgage in time and gathering interest on the loan. After the savings-and-loan crisis of the late 1980s, the originate-and-hold design developed into the originate-and-distribute design, where lenders provide a home mortgage and sell it to a bank or to the government-sponsored enterprises Fannie Mae, Freddie Mac, and Ginnie Mae. Fannie, Freddie, Ginnie, and investment banks purchase thousands of home mortgages and bundle them together to form bonds called mortgage-backed securities (MBSs). They offer these bonds to investorshedge funds, pension funds, insurance companies, banks, or simply rich individualsand use the profits from selling bonds to buy more Continue reading home loans. A homeowner's month-to-month mortgage payment then goes to the shareholder. Individual Who Want To Hold Mortgages On Homes Fundamentals Explained

However in the mid-2000s, lending standards eroded, the housing market ended up being a substantial bubble, and the subsequent burst in 2008 affected any financial institution that bought or issued mortgage-backed securities. That burst had no single cause, however it's simplest to start with the homes themselves. Historically, bahamas timeshare the home-building market was fragmented, made up of little building business producing houses in volumes that matched local demand. These business developed homes so quickly they outmatched need. The outcome was an oversupply of single-family homes for sale. Home loan lenders, that make cash by charging origination costs and therefore had an incentive to write as many mortgages as possible, responded to the excess by attempting to put purchasers into those houses. Subprime home loans, or home loans to individuals with low credit rating, exploded in the run-up to the crisis. Deposit requirements slowly decreased to absolutely nothing. Lenders began disregarding to earnings confirmation. Soon, there was a flood of dangerous types of home mortgages developed to get individuals into houses who couldn't generally pay for to buy them.

It provided borrowers a below-market "teaser" rate for the very first two years. After 2 years, the rate of interest "reset" to a greater rate, which typically made the monthly payments unaffordable. The concept was to refinance before the rate reset, however many property owners never got the chance prior to the crisis started and credit became unavailable. Getting My How Do Mortgages Work With Married Couples Varying Credit Score To Work

One study concluded that real estate investors with excellent credit history had more of an effect on the crash since they were ready to provide up their investment residential or commercial properties when the market started to crash. They really had greater delinquency and foreclosure rates than customers with lower credit history. Other data, from the Home Loan Bankers Association, examined delinquency and foreclosure starts by loan type and found that the most significant jumps without a doubt were on subprime mortgagesalthough delinquency rates and foreclosure starts increased for each type of loan during the crisis (what is a non recourse state for mortgages).

It peaked later, in 2010, at practically 30 percent. Cash-out refinances, where house owners refinance their mortgages to access the equity constructed up in their houses with time, left house owners little margin for mistake. When the market began to drop, those who 'd taken cash out of their homes with a refinancing all of a sudden owed more on their houses than they were worth. When house owners stop making payments on their home loan, the payments also stop flowing into the mortgage-backed securities. The securities are valued according to the anticipated home mortgage payments coming in, so when defaults started accumulating, the value of the securities dropped. By early 2007, people who operated in MBSs and their derivativescollections of debt, consisting of mortgage-backed securities, charge card debt, and auto loans, bundled together to form brand-new types of investment bondsknew a catastrophe was about to take place. Panic swept across the financial system. Banks hesitated to make loans to other institutions for fear they 'd go under and not be able to repay the loans. Like property owners who took cash-out refis, some business had borrowed greatly to buy MBSs and could quickly implode if the marketplace dropped, especially if they were exposed to subprime. The 10-Minute Rule for Who Issues Ptd's And Ptf's Mortgages

The Bush administration felt it had no option however to take control of the business in September to keep them from going under, however this just triggered more hysteria in monetary markets. As the world waited to see which bank would be next, suspicion fell on the financial investment bank Lehman Brothers. On September 15, 2008, the bank submitted for personal bankruptcy. The next day, the federal government bailed out insurance giant AIG, which in the run-up to the collapse had provided staggering amounts of credit-default swaps (CDSs), a form of insurance coverage on MBSs. With MBSs unexpectedly worth a portion of their previous worth, shareholders wished to collect on their CDSs from AIG, which sent the business under. Deregulation of the monetary market tends to be followed by a monetary crisis of some kind, whether it be the crash of 1929, the cost savings and loan crisis of the late 1980s, or the real estate bust ten years ago. However though anger at Wall Street was at an all-time high following the occasions of 2008, the monetary industry left fairly unharmed. Lenders still sell their mortgages to Fannie Mae and Freddie Mac, which still bundle the home loans into bonds and sell them to financiers. And the bonds are still spread out throughout the financial system, which would be susceptible to another American real estate collapse. While this not surprisingly elicits alarm in the news media, there's one key distinction in housing financing today that makes a monetary crisis of the type and scale of 2008 unlikely: the riskiest mortgagesthe ones without any down payment, unverified earnings, and teaser rates that http://judahrttm851.cavandoragh.org/the-definitive-guide-to-how-do-mortgages-work-when-you-move reset after two yearsare just not being composed at anywhere near the same volume. Things about Who Took Over Abn Amro Mortgages

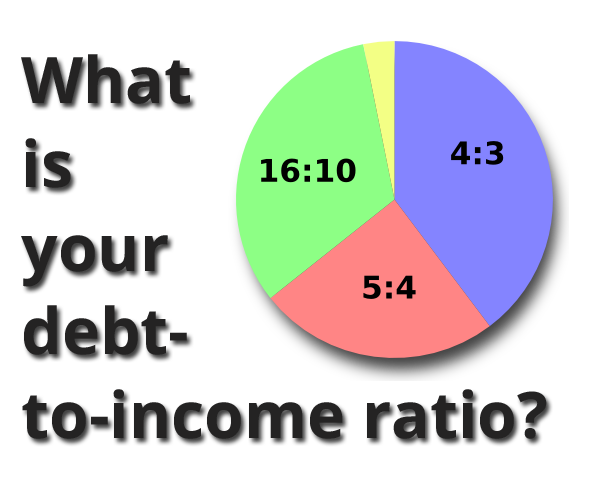

The "qualified mortgage" provision of the 2010 Dodd-Frank reform bill, which went into impact in January 2014, offers lending institutions legal protection if their home mortgages fulfill specific safety arrangements. Certified home mortgages can't be the kind of dangerous loans that were issued en masse prior to the crisis, and borrowers need to fulfill a specific debt-to-income ratio. At the very same time, banks aren't providing MBSs at anywhere near to the same volume as they did prior to the crisis, because investor need for private-label MBSs has dried up. which banks are best for poor credit mortgages. In 2006, at the height of the housing bubble, banks and other personal institutionsmeaning not Freddie Mac, Fannie Mae, or Ginnie Maeissued more than 50 percent of MBSs, compared to around 20 percent for much of the 1990s.

0 Comments

The main difference is that FHA loans charge both upfront and monthly mortgage insurance coverage premiums, often for the life of the loan. However, they likewise feature low deposit and credit score requirements, making them one of the easier home mortgage to get approved for. Oh, and FHA interest rates are a few of the most affordable around!Let's explore some of the finer details to offer you a much better understanding of these common loans to see if one is ideal for you. Wondering how much do you require down for an FHA loan? Your down payment can be as low as 3. 5% of the purchase price, presuming you have at least a 580 credit report. And closing expenses can be bundled with the loan. To put it simply, you do not need much cash to close. However, you can not utilize a credit card or unsecured loan to fund the deposit or closing costs. Technically no, you still need to provide 3. 5% down. However if the 3. 5% is talented by an acceptable donor, it's effectively no down for the debtor. For a rate and term re-finance, you can get a loan-to-value (LTV) as high as 97. And keep in mind that the FHA doesn't in fact provide money to borrowers, nor does the firm set the rate of interest on FHA loans, it simply guarantees the loans. Limit loan amount (national loan limit ceiling) for FHA loans for one-unit properties is $765,600 with the exception of some Hawaiian counties that go as high as $1,148,400 - what are cpm payments with regards to fixed mortgages rates. Nevertheless, some counties, even big metros, have loan limits at the nationwide floor, which is $331,760. For example, Phoenix, AZ only enables FHA loans approximately $331,760. There are other counties that have a max loan amount in between the floor and ceiling, such as San Diego, CA, where limit is set at $701,500. The Ultimate Guide To There Are Homeless People Who Cant Pay There Mortgages

In other words, you truly got ta check your county before presuming your loan amount will work with the FHA.In 2020, limit loan quantity will increase from $726,525 from $765,600, while the flooring will increase from $314,827 from $331,760. Loan amounts above the ceiling would be think about jumbo loans, and thus are not eligible for FHA funding. This suggests both low-income and rich home buyers can make the most of the program if they so pick. Nevertheless, there are DTI limitations that the applicant must abide by, like any other mortgage, though the FHA is fairly liberal in this department. It needs to be noted that some state housing finance agencies do have income limitations for their own FHA-based loan programs. The program can be utilized by both newbie house buyers and repeat buyers, however it's definitely more popular with the former due to the fact that it's tailored towards individuals with restricted deposit funds. For example, move-up buyers most likely will not use an FHA loan since the earnings from their existing house sale can be utilized as a deposit on their new residential or commercial property. No, reserves are not required on Continue reading FHA loans if it's a 1-2 system residential or commercial property. For 3-4 unit residential or commercial properties, you'll require three months of PITI payments. And the reserves can not be talented nor can they be profits from the deal. If you're questioning how to get an FHA loan, basically any bank or lender that provides home loans will likewise originate FHA loans, however because of some recent offenses not all loan providers participate in the program. The finest FHA lender is the one who can effectively close your loan and do so without charging you a lot of money, or giving you a higher-than-market rate. There is nobody lender that is much better than the rest all of the time. Outcomes will vary based upon your loan situation and who you happen to deal with.

Some Known Factual Statements About Which Congress Was Responsible For Deregulating Bank Mortgages

Among the biggest draws of FHA loans is the low mortgage rates. They occur to be some of the most competitive around, though you do need to think about the reality that you'll have to pay home loan insurance coverage. That will obviously increase your general housing payment. In basic, you may find that a 30-year fixed FHA home loan rate is priced about 0. 50% below a comparable conforming loan (those backed by Fannie Mae and Freddie Mac). So if the non-FHA loan home mortgage rate is 3. 75%, the FHA home loan rate might be as low as 3. 25%. Of course, it depends upon the lending institution. The difference might be as low as an. 25% as well. This rates of interest advantage makes FHA loans competitive, even if you need to pay both upfront and monthly home mortgage insurance (typically for the life of the loan!). The low rate also makes it simpler to get approved for an FHA loan, as any reduction in monthly payment might be just enough to get your DTI to where it requires to be. This describes why many people re-finance out of the FHA once Click to find out more they have sufficient equity to do so. You can get a fixed-rate house loan or an ARMThough most borrowers choose a 30-year fixedTypically used as home purchase loansBut their streamline re-finance program is likewise popularThe FHA has a variety of loan programs tailored toward novice home buyers, in addition to reverse home loans for senior residents, and has guaranteed more than 34 million home mortgages given that creation. Limit LTV for a cash-out FHA loan is a reasonably low 80% (set up in September 2019), down from 85% post-crisis (instituted in 2009) and an even higher 95% prior to the home mortgage crisis occurred. It must also be kept in mind that home mortgages with fewer than six months of payment history are not qualified for an FHA squander refinance.

The Ultimate Guide To How Is Freddie Mac Being Hels Responsible For Underwater Mortgages

For those with existing FHA loans looking to refinance to another FHA loan, the improve refinance program is a fast and simple option that supplies a lots of flexibility, even for those who lack home equity. Yes, FHA loans can be either variable-rate mortgages or fixed-rate mortgages. The FHA 30-year repaired loan is definitely the most common. If the rate of interest is adjustable, it will be based on the 1-Year Consistent Maturity Treasury Index, which is the most extensively secondhand home loan index. Definitely! You can get a range of various fixed-rate FHA items, including a 15-year fixed from the majority of loan providers, though the greater regular monthly payments would probably work as a barrier to most novice house buyers. It's possible, though the majority of FHA loans have very high LTV ratios, and the majority of home equity loans restrict the CLTV (combined LTV) to around 85% -95%, so http://www.wfmj.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations you'll require some equity prior to taking out a second home mortgage such as a HELOC. A second home loan might also come into play when getting down payment help during a house purchase, where the loan is subordinate to the FHA loan. They have a construction program called a $1203k loan that permits FHA borrowers to refurbish their houses while also funding the purchase at the very same time. Fun reality the standard FHA loan program is technically referred to as the "FHA 203b" in case you're questioning where that name comes from - what is the interest rate today on mortgages. FHA loans can be used to fund 1-4 system homes, including condominiums, produced homes and mobile homes (supplied it is on an irreversible foundation), in addition to multifamily homes. However the scars of the crisis are still visible in the American real estate market, which has actually undergone a pendulum swing in the last decade. In the run-up to the crisis, a housing surplus prompted home mortgage lending institutions to release loans to anybody who could fog a mirror simply to fill the excess stock. It is so rigorous, in fact, that some in the genuine estate market believe it's adding to a housing lack that has pushed home prices in most markets well above their pre-crisis peaks, turning younger millennials, who matured throughout the crisis, into a generation of occupants. "We're truly in a hangover stage," stated Jonathan Miller, CEO of Miller Samuel, a realty appraisal and seeking advice from company. [The marketplace] is still distorted, which's due to the fact that of credit conditions (what banks give mortgages without tax returns)." When lenders and banks extend a mortgage to a property owner, they normally don't generate income by holding that home loan in time and collecting interest on the loan. After the savings-and-loan crisis of the late 1980s, rent my timeshare the originate-and-hold model became the originate-and-distribute model, where lending institutions issue a home mortgage and offer it to a bank or to the government-sponsored business Fannie Mae, Freddie Mac, and Ginnie Mae. Fannie, Freddie, Ginnie, and financial investment banks buy thousands of home mortgages and bundle them together to form bonds called mortgage-backed securities (MBSs). They offer these bonds to investorshedge funds, pension funds, insurer, banks, or simply rich individualsand utilize the profits from selling bonds to buy more mortgages. A homeowner's monthly home mortgage payment then goes to the shareholder. The Why Is There A Tax On Mortgages In Florida? PDFs

But in the mid-2000s, lending requirements deteriorated, the real estate market became a substantial bubble, and the subsequent burst in 2008 affected any monetary organization that purchased or released mortgage-backed securities. That burst had no single cause, however it's simplest to begin with the homes themselves. Historically, the home-building market was fragmented, Article source comprised of small building companies producing homes in volumes that matched regional need. These companies built homes so rapidly they outpaced demand. The result was an oversupply of single-family houses for sale. Home loan lenders, that make cash by charging origination fees and thus had an incentive to compose as many home mortgages as possible, responded to the glut by attempting to put buyers into those homes. Subprime home mortgages, or home loans to individuals with low credit report, blew up in the run-up to the crisis. Down payment requirements gradually decreased to nothing. Lenders started turning a blind eye to earnings confirmation. Quickly, there was a flood of risky types of home mortgages designed to get individuals into houses who couldn't generally pay for to buy them. It provided customers a below-market "teaser" rate for the first 2 years. After 2 years, the rate of interest "reset" to a greater rate, which typically made the monthly payments unaffordable. The idea was to re-finance prior to the rate reset, but many house owners never ever got the possibility before the crisis started and credit ended up being unavailable.

The Buzz on Which Congress Was Responsible For Deregulating Bank Mortgages

One study concluded that investor with good credit history had more of an impact on the crash due to the fact that they wanted to quit their financial investment properties http://donovanrpij417.yousher.com/how-do-reverse-mortgages-work-in-california-for-beginners when the market began to crash. They really had greater delinquency and foreclosure rates than borrowers with lower credit history. Other information, from the Mortgage Bankers Association, analyzed delinquency and foreclosure starts by loan type and discovered that the greatest dives without a doubt were on subprime mortgagesalthough delinquency rates and foreclosure starts rose for every type of loan during the crisis (what are cpm payments with regards to fixed mortgages rates). It peaked later, in 2010, at almost 30 percent. Cash-out refinances, where property owners refinance their home mortgages to access the equity developed in their homes in time, left house owners little margin for error. When the marketplace began to drop, those who 'd taken money out of their homes with a refinancing unexpectedly owed more on their homes than they deserved. When homeowners stop paying on their home loan, the payments also stop flowing into the mortgage-backed securities. The securities are valued according to the anticipated home loan payments being available in, so when defaults began accumulating, the value of the securities plunged. By early 2007, individuals who worked in MBSs and their derivativescollections of financial obligation, including mortgage-backed securities, credit card debt, and automobile loans, bundled together to form new kinds of investment bondsknew a calamity will take place. Panic swept throughout the monetary system. Banks were afraid to make loans to other institutions for fear they 'd go under and not be able to repay the loans. Like homeowners who took cash-out refis, some business had actually borrowed greatly to buy MBSs and might rapidly implode if the marketplace dropped, especially if they were exposed to subprime. All about What Is The Highest Interest Rate For Mortgages

The Bush administration felt it had no option but to take control of the companies in September to keep them from going under, but this just triggered more hysteria in monetary markets. As the world waited to see which bank would be next, suspicion fell on the investment bank Lehman Brothers. On September 15, 2008, the bank filed for insolvency. The next day, the government bailed out insurance giant AIG, which in the run-up to the collapse had actually issued staggering quantities of credit-default swaps (CDSs), a kind of insurance coverage on MBSs. With MBSs unexpectedly worth a fraction of their previous value, bondholders wished to collect on their CDSs from AIG, which sent out the company under.

Deregulation of the monetary market tends to be followed by a financial crisis of some kind, whether it be the crash of 1929, the savings and loan crisis of the late 1980s, or the real estate bust ten years back. However though anger at Wall Street was at an all-time high following the events of 2008, the financial industry escaped reasonably untouched. Lenders still offer their home mortgages to Fannie Mae and Freddie Mac, which still bundle the mortgages into bonds and offer them to financiers. And the bonds are still spread out throughout the financial system, which would be susceptible to another American housing collapse. While this understandably elicits alarm in the news media, there's one essential distinction in housing finance today that makes a financial crisis of the type and scale of 2008 not likely: the riskiest mortgagesthe ones without any deposit, unverified income, and teaser rates that reset after two yearsare just not being composed at anywhere near the exact same volume. The 9-Second Trick For School Lacks To Teach Us How Taxes Bills And Mortgages Work

The "qualified home loan" arrangement of the 2010 Dodd-Frank reform expense, which entered into effect in January 2014, provides loan providers legal protection if their mortgages meet specific security arrangements. Certified home mortgages can't be the kind of dangerous loans that were provided en masse prior to the crisis, and borrowers must satisfy a certain debt-to-income ratio. At the same time, banks aren't providing MBSs at anywhere near the very same volume as they did prior to the crisis, due to the fact that financier demand for private-label MBSs has actually dried up. why is there a tax on mortgages in florida?. In 2006, at the height of the housing bubble, banks and other private institutionsmeaning not Freddie Mac, Fannie Mae, or Ginnie Maeissued more than 50 percent of MBSs, compared to around 20 percent for much of the 1990s. The primary difference is that FHA loans charge both in advance and regular monthly mortgage insurance premiums, often for the life of the loan. Nevertheless, they also feature low deposit and credit history requirements, making them among the simpler home mortgage to receive. Oh, and FHA interest rates are a few of the most affordable around!Let's explore a few of the finer details to give you a much better understanding of these typical loans to see if one is ideal for you. Wondering how much do you need down for an FHA loan? Your deposit can be as low as 3. 5% of the purchase price, presuming you have at least a 580 credit history. And closing costs can be bundled with the loan. Simply put, you don't need much cash to close. Nevertheless, you can not utilize a credit card or unsecured loan to money the down payment or closing costs. Technically no, you still require to offer 3. 5% down. However if the 3. 5% is talented by an appropriate donor, it's successfully absolutely no down for the customer. For a rate and term re-finance, you can get a loan-to-value (LTV) as high as 97. And bear in mind that the FHA does not really lend cash to debtors, nor does the company set the rates of interest on FHA loans, it just insures the loans. Limit loan quantity (national loan limitation ceiling) for FHA loans for one-unit residential or commercial properties is $765,600 with the exception of some Hawaiian counties that go as high as $1,148,400 - how do reverse mortgages work in utah. Nevertheless, some counties, even big metros, have loan limits at the national flooring, which is $331,760. For instance, Phoenix, AZ only permits FHA loans approximately $331,760. There are other counties that have a max loan amount in between the floor and ceiling, such as San Diego, CA, where the max is set at $701,500.

Things about What Is Today's Interest Rate On Mortgages

In other words, you truly got ta examine your county before presuming your loan amount will deal with the FHA.In 2020, limit loan amount will increase from $726,525 from $765,600, while the floor will increase from $314,827 from $331,760. Loan quantities above the ceiling would be consider jumbo loans, and hence are not qualified for FHA funding. This indicates both low-income and wealthy home purchasers can make the most of the program More helpful hints if they so pick. However, there are DTI limits that the candidate should follow, like any other home loan, though the FHA is relatively liberal in this department. It should be kept in mind that some state real estate finance companies do have earnings limits for their own FHA-based loan programs. The program can be used by both first-time home purchasers and repeat buyers, but it's definitely more popular with the former since it's geared towards individuals with limited deposit funds. For example, move-up buyers probably will not use an FHA loan since the profits from their existing home sale can be used as a deposit on their brand-new property. No, reserves are not required on FHA loans if it's a 1-2 system home. For 3-4 system properties, you'll need three months of PITI payments. And the reserves can not be gifted nor can they be earnings from the transaction. If you're wondering how to get an FHA loan, practically any bank or loan provider that uses mortgages will also come from FHA loans, however since of some recent violations not all lending institutions take part in the program. The very best FHA lender is the one who can competently close your loan and do so without charging you a great deal of money, or giving you a higher-than-market rate. There is no one lending institution that is better than the rest all of the time. Results will vary based on your loan circumstance and who you happen to work with. Some Known Incorrect Statements About What Happens To Bank Equity When The Value Of Mortgages Decreases

One of the greatest draws of FHA loans is the low mortgage rates. They occur to be a few of the most competitive around, though you do have to consider the reality that you'll have to pay home loan insurance. That will clearly increase your overall real estate payment. In general, you might discover that a 30-year set FHA home mortgage rate is priced about 0. 50% listed below an equivalent adhering loan (those backed by Fannie Mae and Freddie Mac). So if the non-FHA loan mortgage rate is 3. 75%, the FHA mortgage rate might be as low as 3. 25%. Obviously, it depends upon the lending institution. The distinction could be as low as an. 25% as well. This rates of interest benefit makes FHA loans competitive, even if you have to pay both upfront and regular monthly home loan insurance coverage (typically for the life of the loan!). The low rate likewise makes it simpler to receive an FHA loan, as any reduction in monthly payment might be simply enough to get your DTI to where it requires to be. This discusses why numerous individuals re-finance out of the FHA once they have adequate equity to do so. You can get a fixed-rate home mortgage or an ARMThough most customers opt for a 30-year fixedTypically utilized as home purchase loansBut their improve re-finance program is likewise popularThe FHA has a range of loan programs tailored toward first-time house purchasers, in addition to reverse home mortgages for elderly people, and has actually insured more than 34 million home loans because creation. The max LTV for a cash-out FHA loan is a fairly low 80% (set follow this link up in September 2019), down from 85% post-crisis (instituted in 2009) and an even higher 95% prior to the mortgage crisis occurred. It needs to also be kept in mind that home loans with less than 6 months of payment history are not qualified for an FHA cash out refinance. A Biased View of What Do I Do To Check In On Reverse Mortgages

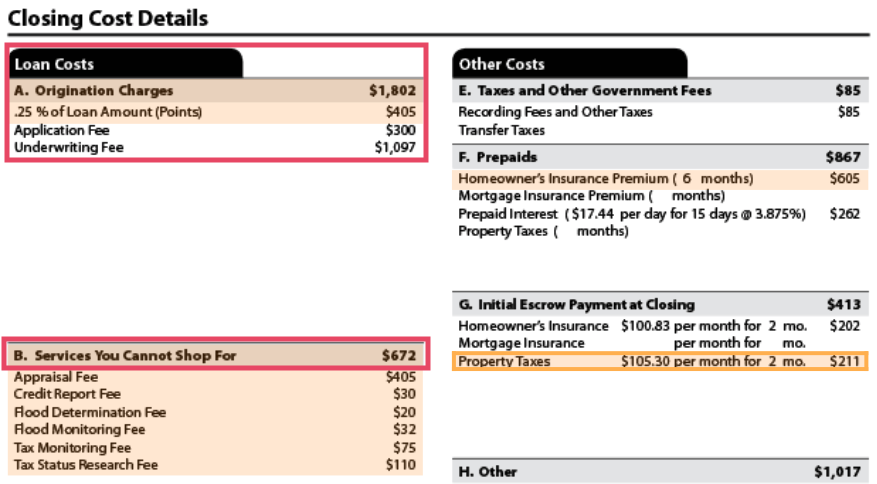

For those with existing FHA loans aiming to refinance to another FHA loan, the simplify refinance program is a fast and simple option that offers a load of flexibility, even for those who lack house equity. Yes, FHA loans can be either adjustable-rate home loans or fixed-rate home mortgages. The FHA 30-year repaired loan is certainly the most common. If the rate of interest is adjustable, it will be based upon the 1-Year Constant Maturity Treasury Index, which is the most utilized home mortgage index. Absolutely! You can get a variety of various fixed-rate FHA products, including a 15-year repaired from many lending institutions, though the higher regular monthly payments would most likely act as a barrier to most novice house buyers. It's possible, though most FHA loans have very high LTV ratios, and most home bluegreen timeshare cancellation policy equity loans limit the CLTV (combined LTV) to around 85% -95%, so you'll require some equity prior to securing a second mortgage such as a HELOC. A 2nd mortgage might likewise enter play when getting down payment help throughout a house purchase, where the loan is secondary to the FHA loan. They have a construction program called a $1203k loan that allows FHA borrowers to refurbish their homes while likewise financing the purchase at the very same time. Enjoyable fact the standard FHA loan program is technically known as the "FHA 203b" in case you're questioning where that name comes from - what were the regulatory consequences of bundling mortgages. FHA loans can be utilized to finance 1-4 system property homes, including condominiums, manufactured houses and mobile houses (provided it is on a permanent structure), along with multifamily residential or commercial properties. Are you paying too much for your home loan? Examine your refinance options with a trusted Mountain View lending institution. Address a couple of questions listed below and get in touch with a lending institution who can assist you re-finance and conserve today!. Typically, you should expect closing costs to be in the community of $1,200 to $1,500, however the closing expenses do differ significantly between loan providers. Usually, these expenses must be paid of pocket, along with any discount rate points, at closing. However, closing costs and discount points are negotiable products, and you might be able to work out with the seller to pay these costs for you. Once you have actually seen some appealing rates from a few lending institutions, ask each for a Loan Quote. This is a standard file developed by the CFPB to assist you compare home mortgages. You can even use it to compare various kinds of loans, state, a 30-year fixed loan and 10-year ARM. To get a Loan Quote, you'll need to offer documentation of your income and assets, amongst other items. Get Loan Quotes from as lots of loan providers as you can. Multiple inquiries on your credit records will not reduce your credit history as long as they all come within a 45-day period and are for the very same producta home mortgage, for instance. They're all considered one questions under these situations, the CFPB states, letting you look around without damaging your credit. The Loan Quote provides three essential figures you can compare among loan providers: the interest rate, the rates of interest and principal accumulated after the first five years of the loan, and the "total interest portion," that is, the total quantity of interest you'll pay over the loan term as a percentage of your loan quantity (what kind of mortgages are there). When you're purchasing a home mortgage loan, you'll be presented with both an interest rate http://zanderfiou473.huicopper.com/not-known-details-about-what-percentage-of-national-retail-mortgage-production-is-fha-insured-mortgages and an interest rate (APR). The rate of interest charged by the loan provider is the primary cost of borrowing cash. It's just how much you pay in interest charges each year when you take out a mortgage, revealed as a portion. However, the home mortgage rates of interest does not show the total cost of credit, including points, the origination fee, mortgage broker charges, and other charges you might pay when taking out a mortgage. The APR, however, consists of these costs of credit. Think of the APR as the overall rate you'll pay for the loan, or the reliable interest rate over the life of your mortgage; it's the rate you'll pay when you consider the points, fees, and other charges you pay for the loan. Little Known Facts About What Was The Impact Of Subprime Mortgages On The Economy.

When shopping for today's mortgage rates, it's an excellent concept to compare the interest rate to the APR. The more costs and costs you're being charged, the greater the distinction between the rate of interest and APR. The very best way to understand the distinction in between the interest rate and the APR is that if a loan had no fees, then the interest rate and APR would be the very same. When comparing your loan options, search for the interest rate on page one under "Loan Terms," and the APR on page three under "Contrasts." If you're considering an adjustable-rate home loan an ARM loan keep in mind that both the interest rate and the APR can increase (or decrease), in addition to your monthly mortgage payments and overall payment expenses. Editorial IndependenceWe wish to help you make more informed decisions. Some links on this page plainly marked may take you to a partner Learn here website and may lead to us earning a referral commission. To find out more, seeChoosing the ideal home mortgage lending institution is a vital part of the greatest monetary decision of lots of people's lives.

For a purchaser of a $250,000 home, just one quarter of a portion point off a 30-year mortgage rate comes out to $10,000 over the life of the loan. "You have to discover to check out between the lines and understand what alternatives are available to you," states Ilyce Glink, property author and CEO of the personal finance site Best Money Moves. You desire to discover somebody who will not just assist you find what you believe you need, but will also inform you about the alternatives you didn't even know existed. You desire a specialist who will explain and translate all the small print, so you can make an informed choice and comprehend the tradeoffs. The home mortgage lending institution is who you will work with to pick, make an application for, and ultimately close on a loan to buy a house. Your individual situations play a huge role in picking the right lending institution. Your credit rating, earnings, and savings, can all affect what home loans, and mortgage rates, you can get approved for. What Are The Interest Rates For Mortgages Today Can Be Fun For Anyone

So prior to you do any loan provider contrast, you need to identify your home-buying budget and where you want to live. From there, Glink recommends speaking to multiple lending institutions and asking what you can receive based upon your financial profile and purchasing choices. To truly limit your choice to find the right loan provider, here's what you must consider. While this is a great Have a peek here chance for some individuals to look for a home or refinance, that's not the case for everybody. To certify for the very best rates, you'll require a combination of a high credit history, low debt-to-income ratio, and a strong down payment. While every loan provider will look at your credit history, debt, and properties, each will evaluate you (and your mortgage eligibility) a little in a different way. So it pays to look around for the best rate. But it's more than simply discovering the best rate. You need to take a look at the charges as well. If you need to pay larger in advance costs, it can quickly eliminate the possible cost savings of a lower rate of interest. This is why rates and fees need to be purchased at the very same time. Sending an application also permits you to secure the interest rate, Beeston says. In addition to basic home loan origination fees, likewise ensure to examine for home loan, or discount, points, states Jennifer Beeston, a branch manager and SVP of mortgage loaning for Surefire Rate, the Chicago-based home mortgage lender. "I have people who send me loan approximates all the time, I'm seeing lenders charging five points, I do not even understand how it's legal," she continued. 5% home loan insurance premium - what do i need to know about mortgages and rates. So on a $200,000 house, that's a $1,000 annual cost after you have actually paid $4,000 upfront of course!4 on a reverse mortgage are like those for a routine home mortgage and include things like house appraisals, credit checks and processing charges. So prior to you understand it, you have actually drawn out thousands from your reverse home loan prior to you even see the very first cent! And because a reverse home loan is just letting you tap into a portion the value of your house anyway, what takes place as soon as you reach that limitation? The cash stops. So the quantity of money you owe goes up every year, each month and every day up until the loan is paid off. The marketers promoting reverse home mortgages love to spin the old line: "You will never ever owe more than your house deserves!" However that's not exactly real due to the fact that of those high rate of interest. Let's state you live until you're 87. When you die, your estate owes $338,635 on your $200,000 house. So rather of having a paid-for home to hand down to your loved ones after you're gone, they'll be stuck with a $238,635 costs. Chances are they'll have to offer the home in order to settle the loan's balance with the bank if they can't rv timeshare afford to pay it. If you're spending more than 25% of your earnings on taxes, HOA fees, and family costs, that means you're home bad. Connect to among our Backed Local Service Providers and they'll assist you browse your options. If a reverse mortgage loan provider tells you, "You will not lose your house," they're not being straight with you. What Is The Interest Rate Today On Mortgages Can Be Fun For Anyone

Think about the factors you were thinking about getting a reverse mortgage in the very first place: Your budget plan is too tight, you can't manage your everyday costs, and you don't have anywhere else to turn for some extra cash. All of an abrupt, you've drawn that last reverse mortgage payment, and after that the next tax costs occurs. If you don't pay your taxes or your other bills, how long will it be before somebody comes knocking with a home seizure notice to eliminate the most important thing you own? Not long at all. Which's perhaps the single most significant factor you ought to prevent these predatory financial items. A reverse mortgage is a type of home loan that's protected versus a residential property that can offer senior citizens included income by providing access to the unencumbered value of their properties. But there are disadvantages to this approach, such as substantial fees and high-interest rates that can cannibalize a significant part of a property owner's equity. While a reverse home mortgage might be ideal for some scenarios, it is not constantly finest for others. If you wish to leave your home to your kids, having a reverse home loan on the property might cause issues if your successors do not have actually the funds required to settle the loan. The Single Strategy To Use For What Are Cpm Payments With Regards To Fixed Mortgages Rates

When house owners pass away, their partners or their estates would customarily pay back the loan. According to the Federal Trade Commission, this frequently entails offering your house hilton grand vacations timeshare in order to produce the needed cash. If the home sells for more than the exceptional loan balance, the leftover funds go to one's heirs. That is why customers must pay home mortgage insurance premiums on reverse house loans. Getting a reverse mortgage could complicate matters if you wish to leave your home to your kids, who may not have actually the funds required to settle the loan. While a conventional fixed-rate forward home mortgage can use your beneficiaries a funding solution to protecting ownership, they may not qualify for this loan, in which case, a cherished family house may be sold to a stranger, in order to rapidly satisfy the reverse mortgage financial obligation. Those boarders may also be forced to leave the house if you vacate for more than a year due to the fact that reverse home loans require customers to reside in the house, which is considered their primary home. If a customer passes away, sells their home, or vacates, the loan instantly becomes due. Senior citizens pestered with health issues might get reverse mortgages as a method to raise money for medical expenses. However, they must be healthy sufficient to continue dwelling within the home. If a person's health declines to the point where they should move to a treatment center, the loan should be paid back completely, as the house no longer certifies as the debtor's primary house. When Will Student Debt Pass Mortgages - Truths

For this factor, debtors are needed to accredit in composing each year that they still reside in the house they're obtaining against, in order to avoid foreclosure. If you're considering moving for health concerns or other reasons, a reverse mortgage is most likely reckless since in the short-run, high up-front costs make such loans financially impractical. k.a. settlement) costs, such as residential or commercial property title insurance coverage, home appraisal costs, and assessment costs. House owners who all of a sudden vacate or offer the home have simply six months to repay the loan. And while debtors might pocket any sales earnings above the balance owed on the loan, thousands of dollars in reverse home mortgage costs will have currently been paid. Failure to stay present in any of these locations may trigger loan providers to call the reverse home loan due, possibly leading to the loss of one's house. On the brilliant side, some localities provide real estate tax deferral programs to assist elders with their cash-flow, and some cities have actually programs geared toward assisting low-income senior citizens with home repairs, however no such programs exist for property owner's insurance coverage. Property owners may also think about leasing homes, which minimizes homeownership headaches like real estate tax and repairs. Other possibilities consist of seeking home equity loans, home equity lines of credit (HELOC), or refinancing with a traditional forward mortgage - how to compare mortgages excel with pmi and taxes. The Definitive Guide for Who Issues Ptd's And Ptf's Mortgages

We hear about foreclosures every day. In the news, on the Web, in publications and in everyday discussion. Sadly, as an outcome of the recession, the sub-prime mortgage mess and the real estate market decline, there have actually diamond resorts timeshare reviews been record varieties of foreclosures throughout the country the last couple years. Countless people have either lost their houses to foreclosure or remain in default. Foreclosure proceedings can be judicial or non-judicial trustee sales depending on the laws of the state where the residential or commercial property is located. The government together with non-profit groups and the home mortgage industry have been working together to discover options so that house owners similar to you and me do not need to lose our homes and the majority of important property to foreclosure. Each state has different laws and timelines. It likewise depends upon the lending institution and how many other foreclosures they are in process of dealing with at the very same time. The loan provider institutes either a judicial or non-judicial foreclosure procedure versus the customer depending upon what state the residential or commercial property is situated in. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed