|

Servicing charges are less usual today than in the past, yet some lenders might still charge them to cover the cost of servicing the reverse mortgage in time. Maintenance costs, if billed, are normally around $30 each month and also can be permitted to accrue onto the lending balance (they don't require to be paid out of pocket). The preliminary rate of interest, or IIR, is the real note rate at which interest accrues on the exceptional loan balance on an annual basis. For adjustable-rate reverse mortgages, the IIR can alter with program limits approximately a lifetime interest rate cap.

Adjustable-rate reverse mortgages commonly have rate of interest that can change on a month-to-month or annual basis within specific limitations. In addition, there may be expenses during the life of the reverse home mortgage. A month-to-month service fee may be put on the equilibrium of the funding (for instance, $12 each month), which then compounds with the principal. Exclusive reverse mortgages are personal financings that are backed by the business that develop them. If you have a higher-valued home, you may get a larger funding advancement from a proprietary reverse home mortgage. So if your residence has actually a higher appraised value and you have a tiny mortgage, you could qualify for more funds. What's A Reverse Home Mortgage?

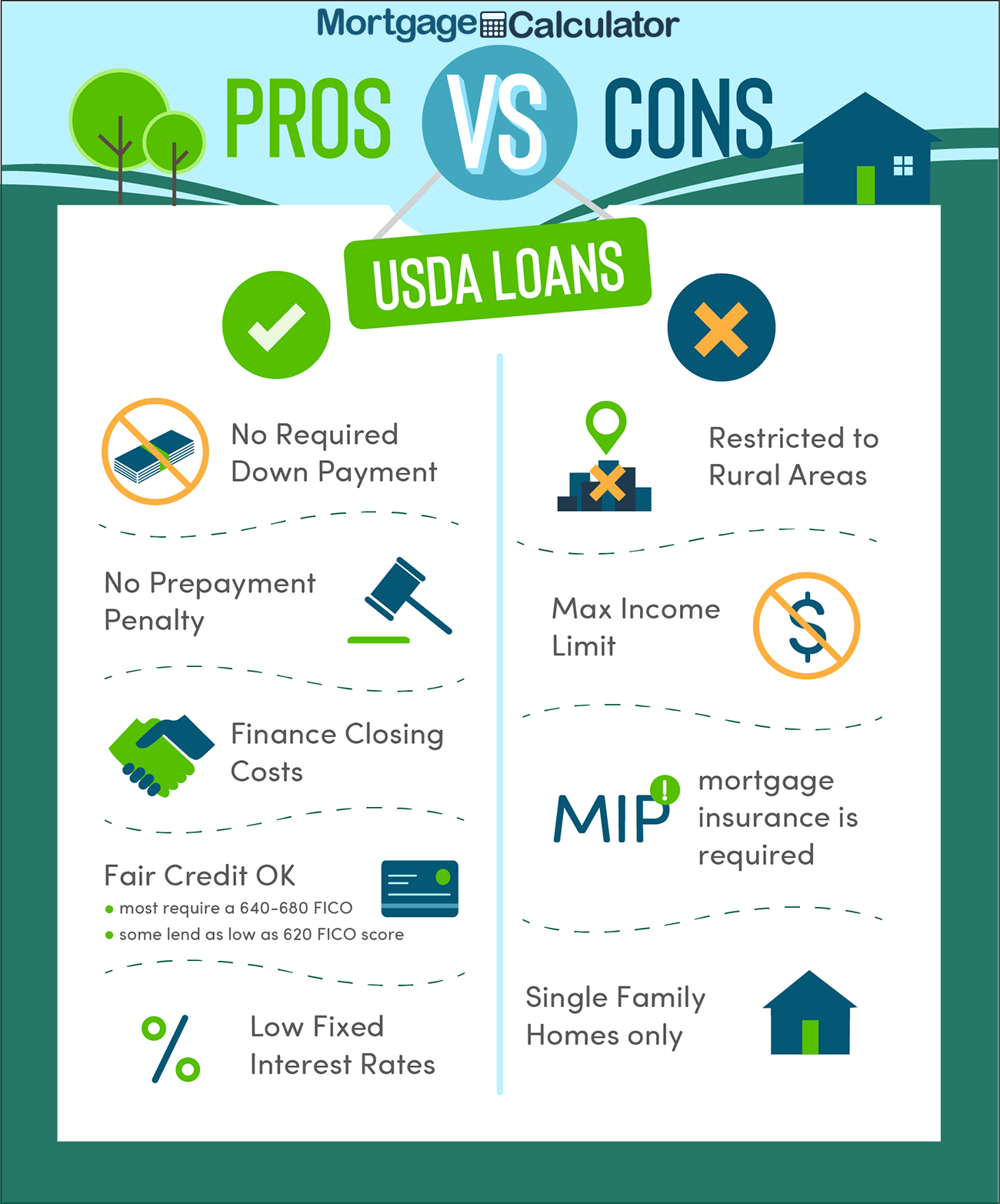

Back then, the debtors can either pay off the financing and maintain the residential or commercial property or sell the home as well as use the earnings to settle the finance, with the sellers keeping any earnings that stay after the finance is repaid. Like various other government lendings, like USDA or FHA loans, these items have guidelines that standard home mortgages don't have, because they're government-insured. These consist of qualification criteria, underwriting processes, funding options as well as, in some cases, limitations on uses of funds. There are additionally personal reverse home mortgages, which do not have the very same strict eligibility requirements or borrowing criteria. Pros & Cons Of Reverse Home Loans

If you have plans to relocate later on in retirement you need to take a look at choices such as the reverse home mortgage for house purchase, or various other residence equity car loans. While you are not called for to make monthly payments, doing so might minimize your regular monthly interest or avoid it from accruing completely. If you choose not to make a month-to-month settlement on the loan, passion for that month will obtain contributed to the complete lending equilibrium. If an individual or business is pressing you to sign an agreement, for example, it's most likely a warning. Reducing expenditures-- Trimming optional expenses can help you remain in your home long-lasting. If you need help with a necessary expense, take into consideration contacting a neighborhood help company, which may be able to aid with gas payments, energy costs and also needed house repair work. Source charge-- To refine your HECM funding, loan providers charge the better of $2,500 or 2 percent of the initial $200,000 of your residence's value, plus 1 percent of the quantity over $200,000. " Typically, the property owner or recipients are not responsible for any kind of expenses if the house is sold for less than the quantity owed," includes Sullivan. Just like any kind of various other sort of home mortgage, you possess the house in a reverse mortgage situation. You can make regular monthly repayments, you can pay quarterly, bi-monthly, semi-annually or simultaneously. Additionally, the line More helpful hints of credit scores expands in availability on the extra funds over time. This indicates that the longer you have funds available on the line, the more money will be readily available to borrow later on need to you require them. If you never draw the cash, you never ever accrue any kind of interest on the funds as well as you, or your successors do not require to repay them. The best amounts usually go to the earliest proprietors staying in one of the most expensive homes obtaining car loans with the lowest expenses. They Click here for info are paid back completely when the last living consumer passes away, offers the home, or completely moves away. Each reverse home mortgage lending institution might have their very own meaning of back-pedaling a reverse home loan. Single-purpose reverse mortgages are the least costly choice. They're offered by some state and also local government agencies, in addition to non-profit organizations, yet they're not available anywhere. These finances might be made use of for just one function, which the lending institution specifies. For instance, the lending institution may state the loan may be utilized just to spend for residence fixings, improvements, or real estate tax. Most house owners with reduced or moderate earnings can get approved Continue reading for these financings. A strong reverse home loan monetary analysis increases the proceeds that you'll obtain due to the fact that the lending institution will not withhold part of them to pay real estate tax as well as homeowners insurance on your behalf.

You can choose routine monthly repayments for as lengthy as you or a co-borrower reside in the residence as your main house. When you and your spouse are co-borrowers on a reverse home mortgage, neither of you need to pay back the mortgage up until you both vacate or both die. Even if one partner relocate to a long-term treatment facility, the reverse mortgage does not need to be repaid till the second spouse leaves or dies. You can access your residence's equity without marketing your home or making month-to-month home loan repayments. Reverse mortgage options can come in the form of cash, a credit line or a basic lump sum of cash-- depending upon which direction you go in. You can use it for house fixings or debt payments, unless your car loan conditions restrict you to a particular cause.

0 Comments

The benefit of selecting a broker is you do less of the work and you'll also get the benefit of their lender knowledge. As an example, they may be able to match you with a loan provider that's fit for your loaning requires, this can be anything from a low deposit home loan to a jumbo home mortgage. Nevertheless, relying on the broker, you could have to pay a charge. The average APR for the benchmark 30-year fixed-rate home mortgage fell to 3.41% today from 3.42% yesterday. Meanwhile, the ordinary APR on the 15-year fixed home loan is 2.78%.

Bankrate's home loan calculator can aid you approximate your month-to-month home loan payment based upon a variety of variables. You can input different house rates, deposits, finance terms and rate of interest to see just how your month-to-month repayment adjustments. The monthly payment estimates show major and rate of interest based upon current home mortgage rates, real estate tax as well as homeowners insurance. You can also factor in your credit history range, ZIP code and also HOA fees to offer you a more exact payment estimate. Obtain The Very Best Prices

When discovering present home mortgage prices, the primary step is to decide what sort of mortgage finest suits your objectives and budget plan. The https://www.timeshareanswers.org/blog/is-wesley-financial-group-llc-legitimate/ majority of debtors opt for 30-year mortgages, however that's not the only selection. Usually, 15-year mortgages have reduced prices however larger monthly payments than the much more popular 30-year home loan.

Discovering The Right Lender

The rate of interest is just the amount of passion the lender will charge you for the financing, not consisting of any one of the administrative expenses. Step 1-- Examine your car loan needs and choose an ideal lender based on variables like mortgage loan rate of interest, payment adaptability, etc. The EMI Calculator is a handy device that assists individuals identify an ideal funding quantity and also tenure that keeps monthly repayments inexpensive. Consequently, make sure to account for rising rates of interest when intending your financing. A buydown is a mortgage funding method where the buyer tries to obtain a lower rate of interest for at the very least the home mortgage's very first couple of years however possibly for its lifetime. A mortgage is a financing normally utilized to buy a home or various other item of realty for which that residential or commercial property then functions as security. ARMs are suitable for borrowers who anticipate to move before their initial price adjustment. This is an added cost paid by the consumer, which protects their lender in instance of default or foreclosure. If you have the ability to make a20 percent deposit, you https://www.timeshareanswers.org/blog/why-are-timeshares-a-bad-idea/ can avoid spending for home mortgage insurance. Splitting your home mortgage lets you profit of a variable price where you can make ... This unpredictable nature might necessitate some factor to consider, particularly if prices maintain increasing. Relying on your car loan problems and your lender, you have the selection to alter over to a different sort of car loan.

Additionally, many fixed-rate investments, like ensured interest choices or assured investment certifications, might provide you greater returns. You can also collaborate with a consultant to update your mutual funds and segregated funds policy to assist you https://landenicpq973.substack.com/p/reverse-mortgage-meaning?r=17w75q&utm_campaign=post&utm_medium=web benefit from higher interest rates. After ending the bond purchases, the Fed is anticipated to elevate the federal funds rate for the very first time since 2018. Student Cash

Charge card prices are variable, yet not typically explicitly connected to the base rate, so won't immediately go up. Card carriers can normally transform prices as and also when they desire-- just recently, for instance, American Express introduced it would certainly be charging its The original source cardholders extra, condemning the increasing price of using rewards. A number of million homeowners are now unmortgaged, many thanks to years of low rates as well as enforced conserving during lockdowns. For them the price rise will have no influence on their housing expenses. If you are wanting to secure an individual loan after a rate of interest rise, you may locate the price of new borrowing has raised. Rocket Mortgage

A home mortgage price lock keeps your rates of interest from changing while you plan for closing. Discover more concerning this form of protection with our full overview. The Fed is really interested in MBS getting because, relying on the year, housing composes 15-- 18% of general financial growth. For example, a mortgage deal might have a 2.09% rates of interest and come with a ₤ 999 product cost. Currently, imagine that it's a year later and rates of interest are greater. The very same $1,000 bond financial investment can net you a 3% yearly interest rate. While the Bank of England base ratedoes play a part, there's not actually a clear link in between Visit this page the base price as well as what lending institutions need to pay to get their funding. If you have a settlement mortgage- which the majority of people do - you'll pay a collection quantity of your equilibrium back every month plus interest on top of that. While it might not feel like a whole lot, a reduced rates of interest also by half of a percent can amount to considerable financial savings for you. Mortgage annual percentage rate represents the overall expense of borrowing a home mortgage, as well as is expressed as a percent. A mortgage interest rate-- which is likewise revealed as a portion-- is the base price you're charged to obtain your lending.

This guarantees you do not miss your due date and pay your impressive balance on schedule. If you miss your payment, you will be billed a fine charge. Many banks require you to submit either domestic or commercial property as security. In some cases, you can additionally promise your plot of land as security. You can not utilize your industrial or farming residential property as safety and security for a LAP. Both residential and business residential properties are accepted as security for home loan. Exactly How Do I Compare Present Mortgage Prices?

View sites for Single-Family Division Single-Family Department Insights, items, as well as modern technology to aid you expand your service. We'll take you detailed via the entire homebuying process. This web page belongs to Purchasing a House, the CFPB's collection of devices and also resources for property buyers. So if the base price rises by 0.5%, your price will increase by the exact same quantity. Amerisave Mortgage Company: Ideal For Refinancing

With this distinction sorted, you can make an application for a finance versus home with Bajaj Finserv as it features no end-use limitation. Mortgage Loans come with longer repayment periods than personal advances. Action 2-- Meet the eligibility demands and inspect cost with a mortgage loan EMI calculator. Candidates must satisfy the following qualification standards to look for a mortgage loan. A 5-year mortgage Visit this site term, at 66% of all home mortgages, is by far the most common duration. You get up to 60% of your residential or commercial property's market price as the approved finance amount. Converting your lending to an additional variation will certainly bring in a conversion cost of 0.50% on your impressive limit plus any extra relevant tax obligations. The maximum amount you can borrow is Rs.10 crore as well as the maximum period of the loan can extend as much as 15 years. In situation of non-payments for a particular month, you will be https://rocketreach.co/wesley-financial-group-email-format_b5a30097f67734a2 billed a 2% penal passion over and above your existing rates of interest. You will certainly have to pay up to Rs.5,000 as a booking fee for this funding. You can get up to 70% of your property's market price sanctioned as the finance. Fixed

To illustrate, allow's look at a $250,000 home loan with a 30-year term, and the differences in payment in between a rate of interest of 4% and a price of 4.25%. Discovering the appropriate home mortgage bargain for you isn't only regarding locating the most affordable rates of interest. The most effective offer involves discovering the right combination of interest rate and costs for you, and recognizing just how to compare offers so you can select the appropriate one for your circumstance. A significant element of APR is home mortgage insurance coverage-- a plan that safeguards the loan provider from losing cash if you back-pedal the home loan. What you can regulate are the quantity of your deposit as well as your credit report. On the various other hand, for several senior citizens, a reverse home loan offers the possibility to maintain a comfortable way of life. This type of finance gives debtors accessibility to the equity they have actually developed, while still possessing as well as living in your residence-- without compulsory regular monthly home mortgage repayments. Nonetheless, as with any type of mortgage, you need to meet your financing responsibilities, maintaining current with property taxes, home owners insurance, maintenance and also any kind of home owners association fees. This is not a complimentary give or a special program that profits elders without there being charges included. The financial institution you deal with needs to wesley llc make charges to pay its workers and to keep its lights on. Reverse mortgages are a lot more pricey than a standard home equity credit line (HELOC-- house equity lending) but it is likewise more affordable than doing a realty transaction such as selling/buying a house.

These products are intricate as well as all costs, benefits, and also negative aspects must be meticulously pondered within the context of your overall economic plan. Suppliers market the advantage of using a reverse home mortgage to boost financial savings by moving wealth from your residence to your financial investments. Basically, a reverse home mortgage could cause you to violate property restrictions for the Medicaid and Supplemental Safety Revenue programs. This is complicated stuff, so make certain to speak with a lawyer that specializes in elder regulation or a legal center prior to looking for a reverse home mortgage program. By signing up to be a participant of Realty Champions, you'll get accessibility to our 10 ideal suggestions as well as new investment suggestions on a monthly basis. Figure out exactly how you can start with Realty Champions by clicking here. Participate in a HUD-approved counseling session, where you gather details about what reverse home mortgages involve. However, reverse home mortgages included significant threats that are frequently underappreciated. Reverse mortgages are established so that the lending institution will get its money back or end up possessing the residence. Also if you adhere to all components of the home mortgage agreement, it's most likely you won't have much money or equity left when the funding schedules, and you'll likely lose the building.

Nobody paid you $3,500, you just have more money readily available to you now. In the second year your development would be based upon the new equilibrium as well as the rates of interest basically back then. If you had a bank card with a restriction of $10,000 as well as the lender elevated your limitation to $20,000, you would certainly have more cash available to spend, however they didn't provide you $10,000. The bank does not pay any kind of rate of interest to the consumer on any type of loan. I would certainly go as far as to claim that if you pick to do this, pay back virtually the whole amount owed however leave a very little equilibrium of simply a pair hundred bucks on the funding unsettled. Reverse mortgages can likewise feature variable rates of interest so your overall expenses can enhance later on. Furthermore, to get a reverse home loan, you have to remain current on your property taxes, keep paying your property owners insurance, as well as make any kind of HOA repayments you're responsible for. If you no more require the extra earnings offered by a reverse home loan as well as can afford to make a monthly home mortgage settlement, you can refinance your reverse home mortgage with a standard loan. Warning: Reverse Home Mortgage Drawbacks & Disadvantages

With a normal mortgage, the debtor gets a funding from a lender as well as pays it back over time. With each repayment, you develop equity in the mortgaged property, and the financing equilibrium decreases. With a reverse home loan, you borrow cash using your home to safeguard the loan, like a routine mortgage. Yet rather than obtaining an in advance lump sum that has to be gradually repaid, you obtain Hop over to this website repayments from the lender, which come to be the car loan. Any kind of non-borrowing individual, consisting of a non-borrowing spouse, must have a plan to repay an Equity Elite reverse home loan upon the consumer's death or any type of other maturity event. The FHA HECM program has protections in place for certain non-borrowing celebrations, so a reverse home loan candidate http://zandertnjg012.wpsuo.com/introduction-of-home-mortgage-rate-of-interest-trends with specific non-borrowing parties should strongly consider a FHA-insured HECM financing. Money

With a reverse mortgage, you can supplement a diminished revenue as well as remain to pay your costs. With our instance $100,000 home loan, the debtor pays about $443 monthly. Of this amount, around $160 is paid towards principal in the initial month to decrease the car loan equilibrium. The rest of the payment-- around $283-- is rate of interest, or what the loan provider fees you for lending you cash. If You Still Can Not Afford The Tax Obligations As Well As Insurance, You Need To Consider Various Other Choices

Some families could be able to avoid actually utilizing a reverse mortgage. A customer of McClanahan's produced his own version, in which he paid his father to help with his living expenses. Other setups are the proprietary reverse home mortgage, a private finance backed by a business, and the single-purpose reverse home mortgage offered by some state or local government companies. Offer benefits and drawbacks are established by our content group, based on independent research. †If component of your car loan is held in a credit line upon which you might attract, after that the unused part of the line of credit scores will grow in size monthly. The growth price is equal to the amount of the rate of interest plus the yearly home loan insurance coverage premium rate being charged on your car loan. If you're 62 or older, there is a house equity line of credit alternative that provides higher economic versatility than a traditional House Equity Line of Credit. It's called a House Equity Conversion Home loan credit line. If there's enough money left over after the sale, your beneficiaries will receive this. However, if the balance is expensive, there might be nothing left. Additionally, there's the loss of an asset that might have heavy nostalgic worth to your loved ones. This suggested that FHA lending prices would vary relying on the can you get out of a timeshare FHA-backed loan provider. Thus, it pays to look around for different lending institutions while trying to find an FHA home mortgage to compare rates. On the various other hand, because standard lenders are usually a lot more affordable, they usually supply reduced rates than FHA fundings. The amounts offered above for Estimated Overall Closing Prices, are estimates based on the state chosen. The actual charges, expenses and also regular monthly repayment on your specific financing purchase may vary, as well as may consist of city, area or other added fees and also prices. When searching for the best rates, consider a variety of loan providers, like neighborhood financial institutions, national banks, lending institution, or online loan providers.

A price and term refinance could reduce your rates of interest and minimize your regular monthly settlement. A variety of FHA variable-rate mortgages are readily available with initial fixed-rate durations of one, 3, 5, 7 or ten years. As soon as the preliminary fixed-rate period ends, the lending will change, meaning your rate and repayment might increase or fall for the rest of the car loan term. For home loan, omitting house equity lines of credit, it consists of the interest rate plus other charges or costs. Acquiring a residence can be a fascinating and also brand-new procedure for lots of people. If your goal is to purchase a house with a very little down payment and low-interest rates, FHA lending rate of interest might be the ideal fit. As an example, a great mortgage rate for somebody that has a reduced credit report often tends to be greater than for a person who has a higher credit score. Our home mortgage rate table is made to help you contrast the rates you're being supplied by lending institutions to know if it is far better or even worse. These prices are benchmark rates for those with great debt and also not the intro prices that make everybody think they will certainly obtain the most affordable rate. offered. Are fees you pay the lender upfront in exchange for a reduced interest rate. Buying down the rate with discount factors can save you money if you're intending on maintaining your house for a long period of time. Mortgage Prices

On the various other hand, a reduced DTI ratio means you're a low-risk consumer with good monetary standing. Despite having sudden emergencies, you are more probable to maintain making home mortgage repayments as concurred. When it comes to down payment requirements, anticipate to make a greater deposit on a standard westland financial services inc loan than an FHA home loan. The majority of conventional lending institutions favor 20% down, though standard lenders approve reduced down payments. While it's a large sum, it will help you bypass exclusive mortgage insurance coverage. On the various other hand, numerous property buyers supply less than 20% down, which requires them to pay PMI for a limited time. Fha Prices Near Half A Century Low!

The repayment quantity does not consist of homeowner's insurance or property taxes which have to be paid in addition to your finance payment. In complete interest, you 'd pay $57,466 over the life of the lending. Also referred to as price cut points, this is a single fee or prepaid interest debtors purchase to decrease the rate of interest for their home mortgage. An FHA car loan is a type of home loan insured by the Federal Real Estate Management. It enables customers with low credit history to get a home with a down payment as reduced as 3.5%. FHA funding guidelines are more forgiving than traditional financings, giving consumers with spotty credit histories and little cash Learn more here money saved for a deposit a shot at homeownership. The ordinary price for a 30-year fixed home loan is 3.090% as of September 27, 2020-- well listed below what rates were for this kind of home loan even one week ago. While home mortgage prices frequently fluctuate, experts expect FHA lending prices to stay reduced in the near future due to the economic hits the country maintained from COVID-19. FHA home loan prices can be more than traditional home mortgage rates. Likewise, if you opt out of on the internet behavioral marketing, you may still see advertisements when you sign in to your account, as an example with Electronic banking or MyMerrill. These ads are based on your details account partnerships with us. We request your e-mail address to ensure that we can call you in case we're not able to reach you by phone. If you're worried regarding obtaining marketing e-mail from us, you can update your personal privacy choices anytime in the Privacy and Safety location of our web site. We want to offer you money, yet we likewise need to pay individuals that make it occur. Be wise when it involves your FHA funding and also your financial future. The strength of the housing market contributes in rates of interest adjustments. When there's a huge need for houses, loan providers bill greater rates of interest. When the demand for houses is low, reduced rate of interest lure potential house buyers. Minimum down payments on an FHA funding can be also smaller sized, making FHA mortgage insurance a built-in necessity for this financing structure. Your debt-to-income ratio is the percentage of your revenue which goes to paying current financial debts. For a FHA mortgage the optimum qualifying DTI is typically 45%. Make a charge occasionally and pay it off promptly; that keeps the provider from closing your account for lack of exercise (what are reverse mortgages and how do they work). Look at your credit mix: If you have only credit cards or only installment loans, consider including the other type so you can show an excellent payment record across varied line of credit (what is the interest rate on mortgages). While you're working your way towards the credit score required to buy a house, check your progress with a complimentary score; some credit cards and lots of individual financing sites offer them. (NerdWallet uses afree credit history that updates weekly.)Free credit report typically are VantageScores, a rival to FICO. Either kind of rating can wesley timeshare cancellation reviews be used to track your development they both emphasize the very same aspects, with minor distinctions in weighting, so they tend to relocate tandem.

If you desire to see where you stand on those so you understand exactly what home mortgage lending institutions will see, you'll need to acquire a comprehensive FICO report. You can http://garrettsvsq028.bearsfanteamshop.com/our-individual-who-want-to-hold-mortgages-on-homes-ideas do that at myFICO.com, then cancel the monthly service instead of pay an ongoing cost. Make certain to cancel prior to the next billing cycle starts; the regular monthly timeshare warrior membership charge will not be prorated. A Mortgage Capital Responsibility (MCFO) is a kind of home loan pass-through unsecured general obligation bond that has a number of classes or tranches. MCFOs use cash circulation from a swimming pool of home loans that produce income to repay financiers their principal plus interest. Payments are received from mortgages in the swimming pool and handed down to holders of the MCFO security. MCFOs do not hold a lien on the mortgages held by the security. They are simply obliged by agreement to use the income from the mortgages to pay their financiers. MCFO owners have no legal rights to the actual hidden mortgages, therefore MCFOs are riskier than CMOs. Like CMOs, MCFOs are a kind of mortgage-backed security created through the securitization of individual residential home mortgages that draw interest and principal payments from that specific pool of mortgages. Like CMOs, MCFOs plan home mortgages into groups with different payment qualities and run the risk of profiles called tranches. The tranches are paid back with home loan principal and interest payments in a specified order, with the greatest rated tranches featuring credit improvement, which is a form of security versus prepayment risk and payment default. The stated maturities of MCFO tranches are figured out based on the date when the last principal from a swimming pool of mortgages is expected to be paid off. However maturity dates for these types of MBS do not take into account prepayments of the underlying home mortgage loans and thus might not be a precise representation of MBS dangers. CMOs, MCFOs and other non-agency mortgage-backed securities those mortgage bonds not backed by the government-sponsored enterprises Fannie Mae, Freddie Mac or Ginnie Mae - were at the center of the financial crisis that resulted in the bankruptcy of Lehman Brothers in 2008 and led to trillions of dollars in losses on home loan and millions of homeowners losing their houses to https://www.globalbankingandfinance.com/category/news/record-numbers-of-consumers-continue-to-ask-wesley-financial-group-to-assist-in-timeshare-debt-relief/ default. In December 2016, the SEC and FINRA revealed brand-new guidelines to moisten MBS risk with margin requirements for CMO and related MBS transactions. What Does What Are The Types Of Reverse Mortgages Mean?

A home mortgage pool is a group of home mortgages kept in trust as collateral for the issuance of a mortgage-backed security. Some mortgage-backed securities released by Fannie Mae, Freddie Mac, and Ginnie Mae are referred to as "pools" themselves. These are the simplest type of mortgage-backed security. They are also called "pass-throughs" and sell the to-be-announced (TBA) forward market. Mortgage swimming pools, which are groups of home mortgages, tend to have similar qualities, such as issuance date, maturity date, etc. While mortgage-backed securities are backed by mortgage security with similar characteristics, collateralized debt obligations are backed by collateral with varying qualities. A crucial benefit of home loan swimming pools is that they supply investors with diversity. Home loan pools are made up of home loans that tend to have comparable characteristicsfor instance, they will generally have near the very same maturity date and rates of interest. As soon as a lender completes a home mortgage transaction, it usually offers the home mortgage to another entity, such as Fannie Mae or Freddie Mac. Those entities then package the home mortgages together into a home loan swimming pool and the home mortgage pool then serves as collateral for a mortgage-backed security. A CDO is a structured monetary product that pools together money flow-generating properties and repackages this property pool into discrete tranches that can be offered to investors. A collateralized debt commitment is named for the pooled assetssuch as home loans, bonds and loansthat are basically debt commitments that function as collateral for the CDO. Home loan pool funds benefit investors seeking realty exposure due to the fact that they are a low-risk investment that moves individually of a stock and bonds and provide a predictable month-to-month income. Mortgage pool fund loans are protected by property and are described as tough cash since unlike the majority of bank loans (which rely on the creditworthiness of timeshare foreclosure process the customer), tough cash loans consider the value of the underlying residential or commercial property. Since of their much shorter terms, hard cash loans are less susceptible to being affected by interest rate swings, which implies it is a more predictable and reliable capital. Like discussed above, home loan pool funds differ, where some focus on specific home types, while some are more general. These difference can impact threat and return, so it is very important to research the different home mortgage swimming pools before diving in. Some Known Facts About Hedge Funds Who Buy Residential Mortgages.

There's nothing much better than stepping out your back door on a hot summer day and jumping in your own swimming pool. But be careful when aiming to purchase or refinance a home with a swimming pool. That swimming pool can trigger delays in the mortgage process, or drown your loan application altogether. Stubrud dealt with a customer who wanted a reverse home mortgage, but had an empty, aging swimming pool on the residential or commercial property. Reverse home mortgages follow FHA standards, which are specific about swimming pools. "They do not desire it to be a health hazard or a safety risk that there's a big gaping hole in the ground." So what did the customer do? "How they handled it was that they filled it in," states Stubrud. The pool ceased to exist. There were no other choices for this aging house owner who didn't have the cash to get the pool in working order. But Stubrud states the client did raise an alternative concept. "They actually desired to keep it and they were going have this below ground greenhouse. Many homeowners believe that what's on your property is your service. While that's partly real, you invite scrutiny to nearly every inch of a home when you decide to fund it with the lender's cash. It's real for FHA loans along with any other loan type. It comes down to security. A pool that is a falling danger or is a breeding place for germs is a threat to the health of the occupants. Not to mention it opens the property owner up to claims (find out how many mortgages are on a property). The exact same standards would use to things like a missing stairs outside the back entrance, missing out on hand rails, or exposed lead-based paint. Fixing the swimming pool to get it into working order will enable the loan process to continue. When buying a house, this might be a predicament. It's risky to utilize your own funds to make repair work on a house that's not yours yet especially swimming pool repairs which can range from a few hundred to a few thousand dollars - after my second mortgages 6 month grace period then what. A Biased View of How Does Bank Know You Have Mutiple Fha Mortgages

There may be another way to make repair work, however. "The customer will require to acquire a quote for the required repair work," states Sarah Bohan, VP of Corporate Relations at MSU Federal Credit Union. "If the repair work are set up to occur after the closing, the loan provider will usually ask for to hold 1.

You receive back any cash left over after everything's done. But do not depend on this solution, states Bohan. "Many lenders are unable to enable repair work after the home loan closes since they offer their loans on the secondary market and need to provide the loan within a set timeframe." Ensure your loan provider enables repairs after closing before you concur to buy a house with a decrepit pool. For instance, approximately one in four outstanding FHA-backed loans made in 2007 or 2008 is "seriously overdue," suggesting the borrower has actually missed out on at least 3 payments or is in personal bankruptcy or foreclosure proceedings. A disproportionate percentage of the company's severe delinquencies are seller-financed loans that came from before January 2009 (when such loans got banned from the firm's insurance programs) - blank have criminal content when hacking regarding mortgages. By contrast, seller-financed loans comprise simply 5 percent of the company's overall insurance in force today. While the losses from loans stemmed in between 2005 and early 2009 will likely continue to appear on the company's books for several years, the Federal Housing Administration's more recent books of business are anticipated to be very lucrative, due in part to brand-new danger protections put in location by the Obama administration. It likewise imposed new rules that require debtors with low credit report to put down greater deposits, took actions to control the source of deposits, upgraded the process through which it evaluates loan applications, and ramped up efforts to decrease losses on delinquent loans. As an outcome of these and other modifications enacted given that 2009, the 2010 and 2011 books of organization are together anticipated to boost the firm's reserves by nearly $14 billion, according to current price quotes from the Office of Management and Budget. 7 billion to their reserves, further stabilizing out losses on previous books of organization. These are, obviously, simply projections, but the tightened up underwriting standards and increased oversight treatments are already revealing signs of improvement. At the end of 2007 about 1 in 40 FHA-insured loans experienced an "early period delinquency," indicating the customer missed three successive payments within the first six months of originationusually an indication that lenders had actually made a bad loan. Despite these improvements, the capital reserves in the Mutual Mortgage Insurance coverage Fundthe fund that covers just about all the company's single-family insurance coverage businessare annoyingly low. Each year independent actuaries estimate the fund's economic worth: If the Federal Housing Administration merely stopped guaranteeing loans and settled all its expected insurance coverage claims over the next thirty years, just how much cash would it have left in its coffers? Those excess funds, divided by the overall amount of exceptional insurance coverage, is referred to as the "capital ratio." The Federal Housing Administration is required by law to keep a capital ratio of 2 percent, implying it has to keep an additional $2 on reserve for every single $100 of insurance coverage liability, in addition to whatever funds are necessary to cover expected claims. 24 percent, about one-eighth of the target level. The agency has actually considering that recuperated more than $900 million as part of a settlement with the country's most significant home mortgage servicers over deceitful foreclosure activities that cost the firm cash. While that has actually helped to improve the fund's monetary position, numerous observers speculate that the capital ratio will fall even further below the legal requirement when the agency reports its financial resources in November. 4 Easy Facts About What Mortgages Do First Time Buyers Qualify For In Arlington Va Described

As required by law, the Mutual Home loan Insurance Fund still holds $21. 9 billion in its so-called funding account to cover all of Visit this site its predicted insurance claims over the next 30 years utilizing the most recent forecasts of losses. The fund's capital account has an extra $9. 8 billion to cover any unexpected losses. That said, the company's existing capital reserves do not leave much space for unpredictability, especially given the problem of anticipating the near-term outlook for real estate and the economy. In current months, real estate markets across the United States have actually revealed early indications of a recovery. If that pattern continuesand we hope it doesthere's a great chance the company's financial difficulties will look after themselves in the long run. In that regrettable event, the firm might require some short-term assistance from the U.S. Treasury as it works through the staying uncollectable bill in its portfolio. This assistance would start Additional resources automaticallyit's always belonged to Congress' agreement with the firm, going back to the 1930sand would total up to a tiny fraction of the company's portfolio. how common are principal only additional payments mortgages. When a year the Federal Real estate Administration moves money from its capital account to its financing account, based on re-estimated expectations of insurance claims and losses. (Think about it as moving money from your savings account to your examining account to pay your expenses.) If there's inadequate in the capital account to totally money the financing account, money is drawn from an account in the U.S. Such a transfer does not require any action by Congress. Like all federal loan and loan guarantee programs, the Federal Housing Administration's insurance coverage programs are governed by the Federal Credit Reform Act of 1990, which allows them to https://diigo.com/0mg5q4 draw on Treasury funds if and when they are needed. It's rather impressive that the Federal Housing Administration made it this far without needing taxpayer assistance, particularly due to the financial difficulties the agency's equivalents in the economic sector experienced. If the company does need assistance from the U.S. Treasury in the coming months, taxpayers will still leave on top. The Federal Housing Administration's actions over the previous few years have actually conserved taxpayers billions of dollars by avoiding huge home-price declines, another wave of foreclosures, and countless terminated tasks. After My Second Mortgages 6 Month Grace Period Then What - The Facts

To be sure, there are still considerable dangers at play. There's always a chance that our nascent housing recovery might change course, leaving the agency exposed to even larger losses down the roadway. That's one reason policymakers must do all they can today to promote a broad housing healing, consisting of supporting the Federal Housing Administration's continuous efforts to keep the market afloat. The company has actually filled both functions dutifully recently, assisting us avoid a much deeper economic recession. For that, all of us owe the Federal Housing Administration a debt of thankfulness and our complete financial backing. John Griffith is a Policy Expert with the Housing team at the Center for American Development. When you choose to purchase a house, there are two broad categories of home loans you can select from. You might select a conventional loan. These are come from by mortgage lending institutions. They're either bought by among the significant home loan firms (Fannie Mae or Freddie Mac) or held by the bank for investment functions. This type of loan is guaranteed by the Federal Real Estate Administration (FHA). There are other, specific kinds of loans such as VA home loans and USDA loans. Nevertheless, standard and FHA mortgages are the 2 types everyone can obtain, no matter whether they served in the military or where the property is physically situated. No commissions, no origination fee, low rates. Get a loan estimate instantly!FHA loans permit customers easier access to homeownership. But there's one significant drawback-- they are costly - what are cpm payments with regards to fixed mortgages rates. Here's a primer on FHA loans, how much they cost, and why you may desire to use one to purchase your very first (or next) home regardless. Recovered 18 March 2019. " Mortgage Qualifier Tool". Federal government of Canada. Evans, Pete (July 19, 2019). " Home mortgage tension test rules get more lenient for very first time". CBC News. Retrieved October 30, 2019. Zochodne, Geoff (June 11, 2019). " Regulator safeguards home mortgage tension test in face of push-back from market". Financial Post. Retrieved October 30, 2019. Financial Post. Congressional Budget Workplace (2010 ). p. 49. International Monetary Fund (2004 ). pp. 8183. ISBN 978-1-58906-406-5. " Finest fixed rate home mortgages: 2, 3, five and 10 years". The Telegraph. 26 February 2014. Recovered 10 May 2014. " Demand for set home loans strikes all-time high". The Telegraph. 17 May 2013. Retrieved 10 May 2014. United Nations Publications. p. 42. ISBN 978-92-1-117007-8. Vina, Gonzalo. " U.K. Scraps FSA in Most Significant Bank Guideline Overhaul Since 1997". Businessweek. Bloomberg L.P. Recovered 10 May 2014. " Regulatory Reform Background". FSA web site. FSA. Recovered 10 May 2014. " Financial Solutions Costs gets Royal Assent". HM Look at more info Treasury. 19 December 2012. Obtained 10 May 2014. ( PDF). www. unece.org. owner, name of the document. " FDIC: Press Releases - PR-60-2008 7/15/2008". www. fdic.gov. (PDF). Soros, George (10 October 2008). " Denmark Provides a Model Mortgage Market" through www. wsj.com. " SDLTM28400 - Stamp Duty Land Tax Handbook - HMRC internal manual - GOV.UK". www. hmrc.gov. uk. A house Visit the website equity loan is one method to tap into your house's worth. However because your house is the collateral for an equity loan, failure to repay could put you at danger of foreclosure. If you're considering securing a home equity loan, here's what you need to understand. A house equity loan can offer you with cash in the kind of a lump-sum payment that you repay at a set rates of interest, however only if enough equity is readily available to you. Gradually paying for your mortgage is one way to grow your home equity. And if real estate worths go up in your area, your equity may grow even faster. Your home equity can help you pay for improvements. NerdWallet can show you how much is readily available. A home equity loan offers you access to a swelling sum of cash at one time. The Main Principles Of How To Switch Mortgages While Being

You'll repay the home equity loan principal and interest monthly at a fixed rate over a set number of years. Make certain that you can manage this 2nd home mortgage payment in addition to your present home mortgage, along with your other regular monthly costs. A home equity loan usually enables you to obtain around 80% to 85% of your home's worth, minus what you owe on your home loan. For example, say your home deserves $350,000, your mortgage balance is $200,000 and your lender will permit you to borrow approximately 85% of your home's worth. Increase your home's value ($ 350,000) by the percentage you can obtain (85% or. 85). That gives you an optimum of $297,500 in worth that could be obtained. Credentials requirements for home equity loans will differ by lender, but here's a concept of what you'll likely require in order to get approved: House equity of a minimum of 15% to 20%. A credit history of 620 or greater. In order to confirm your house's fair market price, your loan provider might likewise require an appraisal to determine just how much you're eligible to borrow. Using your house as collateral carries significant danger, so it deserves the time to weigh the advantages and disadvantages of a home equity loan. Fixed rates offer predictable payments, which makes budgeting much easier. You might get a lower interest rate than with a personal loan or charge card. If your current home loan rate is low, you don't have to consider that up. Less versatility than a house equity credit line. You'll pay interest on the entire loan quantity, even if you're using it incrementally, such as for a continuous renovation project. Just like any loan protected by your home, missed or late payments can put your house in jeopardy. If you decide to sell your home prior to you have actually ended up paying back the loan, the balance of your house equity loan will be due. There's still a total loan amount, however you only obtain what you need, then pay it off and obtain again. That likewise suggests you pay back a HELOC incrementally based upon the quantity you utilize instead of on the entire quantity of the loan, like a charge card. The other crucial difference is that HELOCs have adjustable rates. Little Known Questions About Bonds Payment Orders, Mortgages And Other Debt Instruments Which Market Its.

HELOC rates are often marked down at the start of the loan. However after an introductory stage of around 6 to 12 months, the rate of interest generally increases. The U.S. Bank Simple Loan is a fast and hassle-free way for U.S. Bank inspecting clients to obtain as much as $1,000 to look after prepared and unexpected costs. To begin, merely log in to online or mobile banking and select the Simple Loan application from your monitoring account menu. By Philippe Lanctot Updated June 25, 2018 With mortgage terms and options coming in a variety of options, comprehending the distinctions in which home loan interest is determined may conserve you money. how do reverse mortgages work in utah. The distinction in between easy and compound mortgage interest is that simple home loan interest is determined on a day-to-day basis, while compound home loan interest is computed on a monthly basis. An $800,000 home mortgage with a 30-year term and 4 percent rate of interest will have a monthly payment of $4,799. 00 in both circumstances. With a basic mortgage, interest is computed on a daily basis. On your $800,000 mortgage at a 4 percent rate of interest with a monthly payment of $4,799. In this case the daily rates of interest would be. 04/365, or 0. 010959 percent. Using this rate to the $800,000 balance yields an interest charge of $87. 67 daily. This interest charge is used every day till you make a payment, and a new daily interest charge is calculated based upon the decreased principal amount. The rate used to the principal would be. 04/12, or 0. 333333 percent, leading to an interest charge of $800,000 * 0. 00333333 = $2,666. The procedure repeats itself for another month on the new home mortgage balance after your month-to-month home mortgage payment is applied to interest and principal. The interest computation on a compound home loan will be the very same for every single month, as it is based on one month expiring each time a computation is required. Not known Facts About How Does The Trump Tax Plan Affect Housing Mortgages

For instance, interest on a $800,000 home loan balance would be $800,000 * 0. 04/ 12, or $2,666 despite which month it is. For a basic mortgage, nevertheless, interest in February (non-leap year) would be $800,000 * 0. 04/ 365 * 28, or $2,454. 79 Throughout a non-leap year there will normally be little distinction in between the easy and compound home mortgage. The effect of that extra day in February results in an additional interest here charge for the basic home loan. The variance may be thought about negligible however it may deserve noting. If the 30 year, 4 percent, $800,000 home loan were bought on Jan. 1, 2018, it would be settled at the end of December 2047 on the substance basis. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

/find-and-compare-best-mortgage-rates-4148342_FINAL-d90ea8095a49474f90bee793bf4c5918.png)

RSS Feed

RSS Feed